HFMA | Health Care Executives with Unique Skills are Leading Total Rewards Trends

Evolving Executive and Physician Leadership Talent Requirements

SullivanCotter’s Bruce Greenblatt, Principal, and Kim Mobley, Managing Principal, are featured authors in the Winter 2019 issue of HFMA’s Strategic Financial Planning newsletter.

As healthcare organizations continue to operate in a complex and uncertain environment, the following trends are impacting executive and physician leadership talent requirements and total rewards:

- Consolidation activity as organizations expand geographically and increase their scale and service offerings

- Disrupters outside the healthcare sector, including private equity and technology organizations

- Changing payment models with more revenue at risk that often result in lower margins and capital

- Care systems are streamlining operations and clinical activity to realize the promise of larger scope and scale

- Value-based models focus on expanding access, providing a superior patient experience, and delivering high-quality and cost-effective care

To recruit, retain, and engage highly effective leadership in today’s marketplace, organizations must implement competitive total rewards programs. It is important to design rewards strategies that align:

- Executive and physician leadership talent

- Total rewards with market trends and benchmarks

- Total rewards with performance

READ FULL ARTICLE

Modern Healthcare | New CMS Star Ratings Ignore Socio-Economic Factors

Assessing CMS Star Ratings

In a December issue of Modern Healthcare, SullivanCotter helps to analyze how the inconsistent application of peer groups between CMS’s new star ratings and the Hospital Readmissions Reduction program are creating sizable discrepancies in reported performance. By not risk-adjusting hospitals by peer groups based on their dual-eligible population in the latest preview of the CMS star ratings, hospitals with the largest percentage of dual-eligible stays fared worse than others in the readmissions category - hurting their overall star rating.

READ FULL ARTICLE

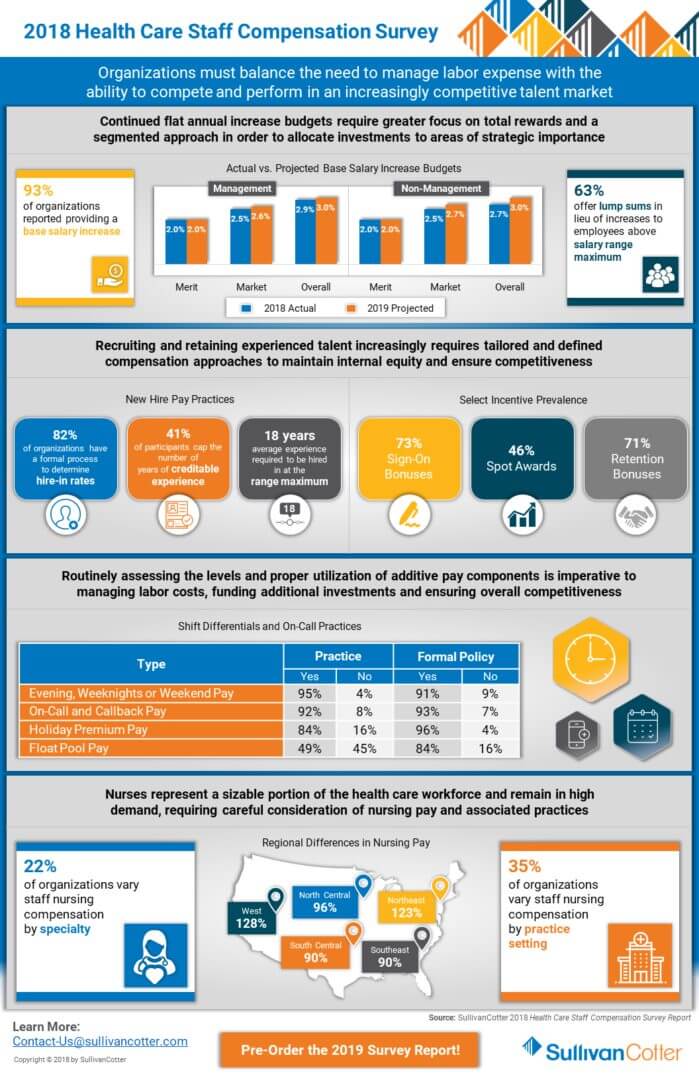

INFOGRAPHIC | 2018 Health Care Staff Compensation Survey

Focusing on compensation and pay practices across the entire health care organization

Health care continues to evolve at a rapid pace, and organizations must balance the need to manage labor expense with the ability to compete and perform in an increasingly competitive talent market. This requires greater focus on compensation and pay practices across the entire health care workforce, including not just executives and providers but staff and other professionals in administrative, nursing, service and supervisory roles as well.

View highlights from SullivanCotter's 2018 Health Care Staff Compensation Survey, featuring data from nearly 600 organizations on 58,000 different health care professionals.

DOWNLOAD INFOGRAPHIC

INFOGRAPHIC | APP Leadership Practices and Structures

Supporting APP retention and engagement

Advanced practice providers (APPs) comprise one of the fastest growing workforces in the United States and are integral to effective and efficient health care delivery.

Organizations are seeing the need for leadership structures and practices to help support this important workforce.

Looking to gain additional insight? Contact us to learn more about developing effective APP leadership practices, structures and compensation strategies to help support your growing APP workforce.

DOWNLOAD INFOGRAPHIC

Split-Dollar Life Insurance: Risks, Benefits and Key Considerations

Delivering cost-effective executive benefits

READ FULL ARTICLE

Health care organizations are facing increased pressure as they try to recruit and retain top talent. At the same time, the onset of the 2017 Tax Cuts and Jobs Act and the introduction of a 21% employer-paid excise tax on compensation over $1 million for top-paid executives has left some hospitals and health systems asking the

following question: Is there a more cost-effective way to deliver compensation and benefits?

These challenges have triggered renewed interest in split-dollar life insurance, although limited adoption rates have been observed to date based on SullivanCotter’s 2018 Benefits Practices in Hospitals and Health Systems Survey Report. While, under certain circumstances, split-dollar life insurance has the potential to reduce costs for the employer while delivering a similar or greater benefit for the executive, it is a much more complex approach than cash-based compensation structures and carries risks that must be carefully evaluated.

For some, split-dollar life insurance evokes memories of past programs that did not deliver on the promises made or, worse, resulted in a cost to the executive rather than a benefit. Proponents of contemporary approaches cite refinements to the design, potential excise tax savings and reductions to operating expenses as reasons to consider such a program. However, a balanced review will also examine the long-term cost impact, inherent complexities, risks, optics, capital requirements and regulatory uncertainty.

The key is understanding the nuances of today’s split-dollar life insurance arrangements and under what circumstances they might warrant consideration.

WHAT IS SPLIT-DOLLAR LIFE INSURANCE?

Split-dollar life insurance is fundamentally different from cash-based compensation programs. Contemporary split-dollar life insurance programs are typically structured as follows:

- In lieu of cash-based programs, the employer funds a life insurance policy with a single up-front premium. This is treated as a loan to the executive where the principal and interest is typically repaid upon death.

- If the loan accrues interest at the Applicable Federal Rate (AFR) and is repaid, it results in no taxable income for the duration of the arrangement.

- The executive can receive tax-free withdrawals from the policy each year during retirement.

- The loan is not considered a cost from an accounting perspective, resulting in reduced operating expenses.

- Since the arrangement is not considered taxable income, excise taxes may be reduced. Legislation specifies that regulations will be prescribed to prevent avoidance of the excise tax. As such, the potential reduction in excise taxes through use of split-dollar life insurance is uncertain, pending excise tax final regulations.

WHAT ARE THE KEY BENEFITS OF SPLIT-DOLLAR LIFE INSURANCE?

The potential benefits of split-dollar life insurance programs are primarily financial in nature:

- Split-dollar life insurance commonly results in reduced operating expenses and, due to the accounting treatment, a shift from investment income to operating income. The long-term cost impact will depend on the investment income opportunity cost relative to the operating gains.

- Availability of retirement income from split-dollar life insurance is typically adjusted to be higher than the alternative cash-based program. Due to the risks involved with split-dollar programs, executives must consider timing, amount of cash flow and potential variability in those amounts when deciding whether or not this arrangement is right for them.

There is no simple way to identify the financial impact without modeling projections under different scenarios. The financial impact can vary significantly based on the size of the loan, the age of the individual, interest rates, life insurance policy features and tax rates. How comparisons are made, including when retirement income is expected to be available and over what period, can have an impact as well.

WHAT ARE THE KEY RISKS ASSOCIATED WITH SPLIT-DOLLAR LIFE INSURANCE?

Any expected financial benefits should be assessed against the following costs and risks associated with split-dollar life insurance:

- Complexity and degree of confidence with impact to executive’s assets. Program tends to be a voluntary alternative to a simpler cash-based program and adopted only by those who can afford to accept the inherent risks.

- Long-term commitment. The program may be in place for several decades, during which time there could be several unanticipated events impacting the program’s performance with no viable exit strategy.

- Retirement income needs and cash flow. Program is only available through regular annual payments and not lump sums. This reduces the ability to adapt to an executive’s evolving financial needs and preferences.

- Corporate cash flow. In many cases, the organization must increase its cash outlay to make the program attractive to potential participants. This can call into question whether tying up additional assets in the split dollar program is a good use of funds by a not-for-profit organization. While there may be financial benefits, the optics could be challenging to defend as the size of loans reportable on the Form 990 Schedule L can be significant – albeit without any reportable income on Schedule J.

- Life insurance policy performance. The success of the split-dollar program hinges on the life insurance policy performance. Policy illustrations include assumptions about market-related factors, such as S&P500 index performance, as well as elements controlled by the life insurance company, including policy charges and crediting rates. Illustrations typically show one scenario based on current policy charges and another based on guaranteed charges – and the results can be substantially different. The ability to maintain current policy charges is contingent on the insurance company’s profitability.

- Plan administration. Few organizations have the infrastructure necessary to administer the program internally and rely instead on outside administrators with associated expenses. Maintaining an understanding of these arrangements within the organization will be important as inevitable staff turnover occurs throughout the life of the program.

HOW SHOULD ORGANIZATIONS PROCEED?

Those interested in pursuing split-dollar life insurance should follow a process that ensures robust analysis and engagement with all stakeholders.

Engage an independent advisor. Many organizations rely on advisors who can financially benefit from the placing of the insurance in the form of commissions. It is rare for organizations to have internal resources to evaluate these programs given how seldom they are currently being used. Acting on the organization’s behalf, an independent advisor can work with the individual brokers to ensure key objectives are being met and the proposals appropriately reflect the costs, benefits and risks of the arrangement. The independent advisor can then provide an assessment of the proposals, ensuring that the organization receives a balanced perspective and understands the critical aspects of the program that impact decision-making.

Organizations should assess these five considerations and reevaluate interest after each step:

- Review of executives who might be suitable candidates and which cash-based programs could be exchanged for split-dollar life insurance. If multiple executives may potentially participate, one or two individuals may serve as test cases.

- Initial engagement with stakeholders to identify the level of interest from executives, the Board’s or Compensation Committee’s perspective on risks and optics, and determination of how program costs will be evaluated by the organization’s finance leaders.

- Identification of one or more experienced insurance brokers who can develop a detailed proposal that supports the key strategic objectives. The proposal should include design features, cost analyses, benefit projections and stress testing of multiple assumption sets.

- Independent assessment of the proposals that ensures a clear, unbiased summary of the program’s operation, impact on operating income/expenses and investment income, considerations for participants, program optics and disclosures, key risks and additional insights regarding assumptions.

- Consideration of the proposals and independent assessment by all stakeholders, including potential participants, Board or Compensation Committee members and finance leaders.

If a split-dollar life insurance program is under consideration, a thorough assessment of potential risks and rewards must be conducted. Having an independent expert who can facilitate the process, deliver a balanced evaluation of options and ensure each party is asking the right questions and getting the answers they need is critical to making an informed decision.

Note that SullivanCotter does not sell insurance or receive commissions, referral fees or payments from those who do.

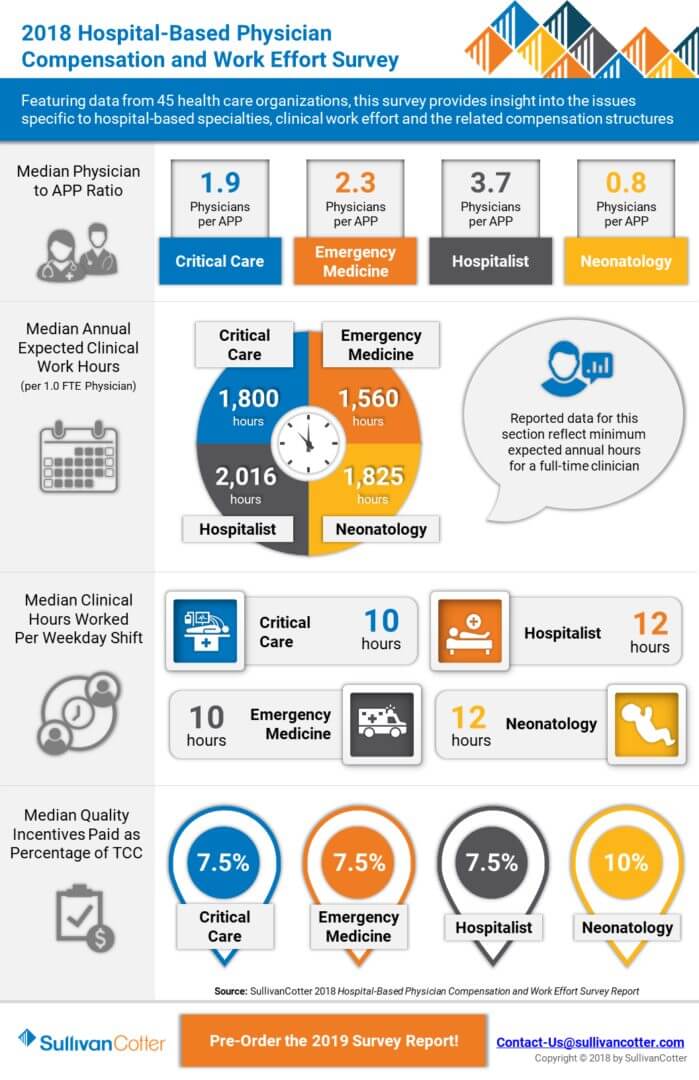

INFOGRAPHIC | 2018 Hospital-Based Physician Compensation and Work Effort Survey

Emerging Trends in Hospital-Based Physician Compensation and Work Effort

Featuring data from 45 health care organizations, this survey provides insight into the issues specific to hospital-based specialties, clinical work effort and the related compensation structures.

View highlights from this year's results and learn more about our Hospital-Based Physician Compensation and Work Effort Survey.

DOWNLOAD INFOGRAPHIC

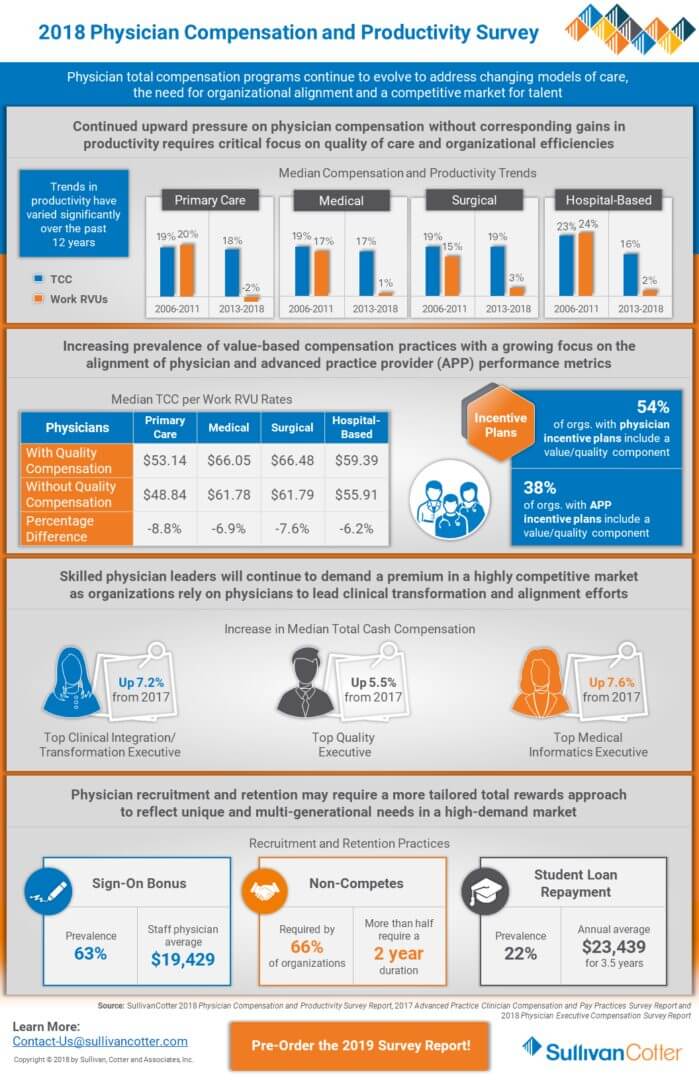

INFOGRAPHIC | 2018 Physician Compensation and Productivity Survey

Benchmarking physician compensation and pay practices

As health care organizations nationwide look to optimize clinical care and ensure financial stability in a highly complex environment, physician compensation programs are evolving to address changing models of care, the need for organizational alignment and a competitive market to talent.

View highlights from SullivanCotter's 2018 Physician Compensation and Productivity Survey, featuring data from nearly 750 organizations covering more than 167,000 individual physicians and advanced practice providers.

DOWNLOAD INFOGRAPHIC

Employers Choose Bonuses Over Raises

SullivanCotter Featured in the Wall Street Journal

In today's competitive talent market, organizations are looking for ways to attract and retain talent while controlling costs. The increasing use of incentives over traditional raises in base pay is trending across all industries. As health care organizations continue to focus on driving performance and enhancing organizational alignment, incentive compensation remains a key component of competitive total rewards programs. SullivanCotter was proud to contribute to this recent article, published in the Wall Street Journal, highlighting this shift in pay practices.

READ FULL ARTICLE

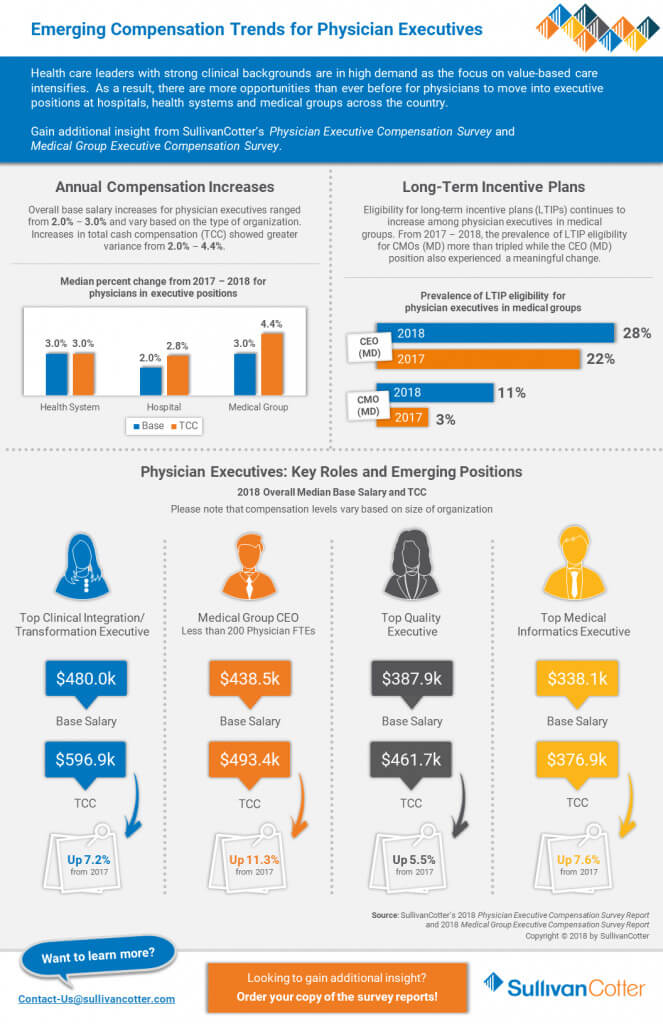

INFOGRAPHIC | Physician Executive Compensation

Emerging Compensation Trends for Physician Executives

Health care leaders with strong clinical backgrounds are in high demand as the focus on value-based care intensifies. As a result, there are more opportunities than ever before for physicians to move into executive positions at hospitals, health systems and medical groups across the country.

Gain additional insight from SullivanCotter's Physician Executive Compensation Survey and Medical Group Executive Compensation Survey.

DOWNLOAD INFOGRAPHIC

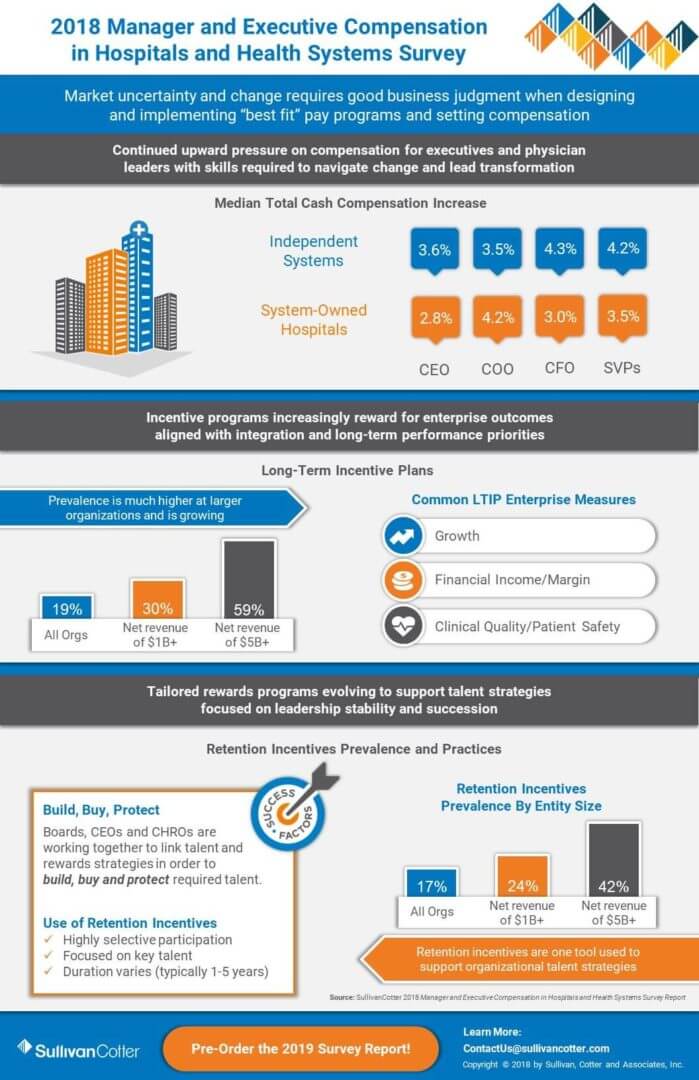

INFOGRAPHIC | 2018 Manager and Executive Compensation in Hospitals and Health Systems Survey

Market Uncertainty and Change Requires Good Business Judgment

In today's unprecedented health care environment, organizations remain focused on two fundamental issues: optimizing clinical care and ensuring financial stability. These new performance priorities are setting the agenda for executive talent and rewards, and require good business judgment when designing and implementing “best fit” pay programs and setting compensation.

Learn more and view highlights from our Manager and Executive Compensation in Hospitals and Health Systems Survey.

DOWNLOAD INFOGRAPHIC

SullivanCotter Hires David Schwietz as Chief Information Officer

Integrating technology solutions, systems and services across the organization

MINNEAPOLIS, Aug. 29, 2018 -- SullivanCotter, the nation's leading independent consulting firm in the assessment and development of total rewards programs and workforce solutions for the health care industry and not-for-profit sector, announces the hire of David Schwietz to serve as the firm's first Chief Information Officer.

"Health care continues to evolve at a rapid pace, and innovation is now the cornerstone of driving efficiency in an industry that is highly focused on improving the total cost of care. To help navigate an increasingly complex operating environment, hospitals and health systems are actively looking to integrate technology solutions, systems and services across the organization. David's longstanding expertise and knack for cutting-edge solutions will play a vital role in helping our clients stay ahead of the curve," said Ted Chien, President and CEO, SullivanCotter.

David has over 25 years of consulting, entrepreneurial and executive management experience and has helped to develop strategy and lead key information technology initiatives at some of the nation's most prominent financial, medical and federal organizations. He also has specialized knowledge in blockchain technology and business intelligence, understanding their potential for transforming the way health care organizations manage, store and secure data.

With a particular focus on enhancing data security, expanding infrastructure to enable firmwide solution and information strategies, and developing new and innovative software services, David is responsible for leading SullivanCotter's technology growth initiatives and related resources in a way that helps to drive greater value for clients.

David joins SullivanCotter from the Federal Reserve Bank of Minneapolis, where he served as the Vice President of Information Technology and was responsible for managing the systems, people and platforms required to ensure the safety and stability of the bank's day-to-day technical operations. He frequently speaks on blockchain and other emerging technologies, and is currently co-authoring a book on artificial intelligence.

About SullivanCotter

SullivanCotter is the leading independent consulting firm in the assessment and development of performance-based total rewards programs and workforce solutions for the health care industry and not-for-profit sector. For over 25 years, the firm has provided unbiased advice to executives and boards to help attract, retain and motivate executives, physicians, advanced practice providers and employees at all levels. Through the Center for Information, Analytics and Insights, SullivanCotter has developed the most widely recognized compensation surveys in the United States. Combining data-driven intelligence with national insights, we act with integrity to help organizations fulfill their missions, business objectives and regulatory requirements.

View Press Release

Modern Healthcare | Annual Executive Compensation Article

Prioritizing performance-based incentive strategies

Providing high-quality care and driving greater value for patients while also keeping costs in check remains one of the greatest challenges for hospitals and health systems nationwide - placing a premium on top executive talent with the skills and experience necessary to lead such efforts.

Amid these ongoing cost-containment initiatives, organizations continue to prioritize executive pay and new performance-based incentive strategies in order to attract, retain and engage leadership and keep pace in a world where the demand for talent outweighs supply.

Learn more from Modern Healthcare's annual executive compensation analysis, featuring data from SullivanCotter's 2018 Manager and Executive Compensation in Hospitals and Health Systems Survey and insights from Kathy Hastings, Managing Director, and Tom Pavlik, Managing Principal.

READ FULL ARTICLE

Q&A | What Comes After Physician Compensation Design?

Developing physician and APP compensation plans

DOWNLOAD FULL ARTICLE

As health care revenue sources continue to shift from volume to value and organizations take on more risk, new physician and advanced practice provider (APP) compensation strategies are emerging. The health care industry is adapting to new payment and care delivery structures with increasingly complex compensation models to match. Organizations must now consider a growing number of components when developing these plans, including recruitment, retention and engagement, patient satisfaction, access, quality of care, governmental regulations and more.

You’ve put time and effort into designing an effective physician compensation plan. How can you make your implementation equally transparent, accurate and successful?

SullivanCotter experts Dr. Mark Rumans, Chief Medical Officer, and Courtney Dutton, Principal, recently answered questions on physician compensation design and implementation - helping to uncover emerging trends and address the increasingly complex challenges health care organizations are facing today.

What are some common challenges organizations face when designing an effective physician compensation program?

CD: Organizations are dealing with a significant number of moving parts when it comes to physician compensation programs. There is both a regulatory environment that focuses on pure productivity and a reimbursement environment that is rapidly changing to focus more on cost efficiencies and value. Because of the proximity of these two realities, along with their varying degrees of complexity, health care leaders often feel like they are living in two different worlds. As organizations start to incorporate more value and quality-based metrics into their plans, physician alignment and engagement becomes more challenging. Historically, physicians have often been isolated relative to the strategic initiatives of the hospital, health system or medical group. But organizations are now recognizing the importance of aligning system-wide goals across all workforces – executives, physicians, advanced practice providers and employees – and must consider a shared vision between each when developing new compensation plans.

MR: It’s very difficult to make changes to physician compensation when the physicians (or the medical group) do not fully understand the reason for the change. Physicians are not always fully aware of all the financial pressures in today’s changing health care environment, and thus don’t understand why change is needed – especially if the physician group is happy with the current program. You need to be able to communicate what you are trying to accomplish and why, and explain how the new compensation plan is aligned with the mission, vision and values of the organization.

After identifying the need for change, the question many organizations struggle with is how far and how fast can you move at any one period of time? Organizations need to consider the gap between current and desired performance and, while they may have some aggressive goals, need to recognize that change to a compensation plan can only move so fast. Significant variation from the current state can cause disruption and unintended consequences if not carefully implemented.

CD: Another common challenge is that the health care industry has been slower to embrace many of the administrative technologies that support infrastructure change and enhanced reporting capabilities of major initiatives such as compensation programs. As a result, there is no clear line of sight for physicians to understand their total performance and how changes in performance can impact their compensation. Right now, physicians are relatively comfortable with the accuracy of their personal productivity as measured in work relative value units (wRVUs). However, as organizations incorporate non-productivity elements into compensation payment models, lack of confidence in the data as well as insight into its impact on outcomes creates challenges when trying to gain physician support for new compensation model.

MR: I agree. Physicians prefer compensation that is related to things they can control or influence - which makes having data points at the hands of a physician so critical. Physicians need a trusted reporting mechanism with accurate and timely data to help track how their actions directly impact their performance.

When you consider some of these common challenges in physician compensation, what key things do organizations need to think about in the design and planning process to help ensure a successful implementation?

MR: I cannot stress enough the importance of compensation committee member selection. Organizations need to include influential thought leaders on the compensation committee who are respected by their colleagues and who can effectively communicate the need for change. Ideally, your compensation committee should include a number of physician leaders who can set aside their personal and departmental compensation and consider the goals of the entire organization. Once your committee has been selected, laying out a framework for success and coming to agreement on what you’re trying to do and why you’re doing it is critical. This can be difficult at first because the committee will not likely have all the technical details about the new plan. Throughout the design process, there are four important things to keep in mind:

- Define the need for change with respect to the shared vision of the organization

- Select the process for change with consideration to what decisions need to be made

- Decide who is going to make these decisions and what data is needed to support them

- Define and begin implementation of a communication plan to providers

CD: Identifying strong physician leaders to champion the change is vital to success. These strong physician leaders need to have an active voice in the development of the compensation plan. Physicians have a front-line care delivery perspective and can speak to issues that may hinder or enhance the move to a performance-based compensation model. Physician leaders who serve on compensation committees need to take ownership of the plan, inform and educate the committee, synthesize data that pertains to the plan and champion the change within the physician workforce throughout the entire process (development, testing, rollout, implementation and annual review).

MR: As medical groups continue to grow, implementing compensation plan changes for groups with 200 or more physicians/providers is no longer an easy task. Imagine doing it with thousands of physicians! So, in addition to strong leadership, the compensation committee must also be mindful of the organization’s ability to implement a new plan from a “nuts and bolts” perspective. They need to assess what type of systems are required to implement the plan well before the plan has been approved. Working out the physical implementation of the plan well in advance of it going live has many benefits and allows you to course correct should there be any technical issues.

Additional questions to consider are:

- What is needed from an IT standpoint to implement the plan?

- What tools do we currently have and what is our capability in regards to reporting performance metrics to physicians in real-time?

- How will comparisons of the current compensation structure to the new model(s) be communicated and what tools are needed to administer this change?

How critical is communication when implementing changes to a compensation program?

MR: Communication is as critical as the plan itself. Committees and administration need to develop a communication plan in tandem with the development of the compensation plan. The questions the compensation committee considers in the plan development will typically be the same questions asked later by providers. Anticipating these questions will help encourage plan adoption, drive engagement and serve as your roadmap to a successful launch.

CD: Building a communications plan at the beginning of a compensation redesign helps set expectations regarding the project’s timeline and identify the major milestones. Once the milestones are identified and agreed upon by the compensation committee, it is important to plan the frequency and mode of communication. Be sure to establish a process to allow for feedback and be flexible should changes need to occur based on that feedback.

MR: What you communicate and how frequently you communicate are also very important factors to consider. An ideal communications plan will allow for several “touchpoints” to share (on paper, in person and electronically) the basics: who, what, where, when, why and how. Equally important is clearly articulating who the decision makers are, and why, to ensure expectations are set as to how feedback will be used throughout the process. You can do some of this communication via email, but ideally your communications plan will allow (early on and throughout the process) for several one-to-one and oneto-many communication opportunities.

Consider the following opportunities in your communications plan:

- Town Hall meetings

- Lunch and Learn presentations

- Dinner with your Chief

- Monthly or weekly communication from the CMO and/or compensation committee

- Online communication (such as a website that outlines the plan and process, stores important documents, Q and A and a managed chat room)

CD: Setting context is an important first step. Providing opportunities for physicians to understand changes in reimbursement and compensation structures and how market influences are impacting and/or apply to your organization is very important. Be prepared to explain your organization’s short-term and long-term strategy and what is driving the need for change. This is where physician champions are key. Allowing them opportunities to reinforce the need for change with peers lays the groundwork for physician engagement and involvement as opposed to a top-down approach when the message is delivered only by administration.

Once the compensation plan is developed and agreed upon, how can an organization drive provider engagement throughout the implementation and transition to a new compensation program?

MR: As new compensation plans are implemented, it is important for providers to have the opportunity to understand what the new performance expectations are and how a change in performance will impact their compensation. Give specific examples and allow physicians time to ‘shadow’ the new plan without any impact to their current compensation. During this shadow period, be able to show where there are gaps in performance and what changes are needed to mitigate any downturns. It is important that physicians understand the organization wants them to be successful and will work with them to understand and close any gaps in performance.

CD: During the shadow period, it is also important to communicate how the plan will be administered once it is fully implemented. This should include how often physicians can expect performance reports, the process for identifying data discrepancies and availability of subject matter experts that can address questions. Additionally, after the completion of the shadow period, many organizations implement a phase-in of the new compensation plan, which provides protection for providers with significant changes in compensation and allows for additional time to adjust behaviors and adapt to the new model.

What are some tactics (or examples) for increasing provider acceptance and support of proposed changes to a compensation program?

CD: Establishing a formal compensation review committee and governance process allows physicians the opportunity to present concerns or raise valid pushback/unintended consequences of the new compensation plan. This committee would be responsible for reviewing the plan on an annual basis to ensure continued alignment with system goals and strategic initiatives, recommending plan changes, reviewing non-productivity metrics and vetting provider or departmental requests for plan modifications.

MR: In addition to establishing a governance process, any tools that make the plan more transparent will help to generate more support. Whether it is a report or online dashboard, you need to how physicians how they are performing and how this relates to the new compensation model. There is often apprehension surrounding this process, and the fear of change is often more harmful than the change itself. Be sensitive to this and utilize as many tools as possible to help make the transition as smooth as possible.

Once the new compensation program is fully implemented, how do you sustain provider engagement?

Continued transparency is vital. The most successful systems allow for ongoing feedback on the program and continue to monitor the impact after it has been fully implemented. Don’t be surprised if subtle program changes are required. Small changes to the plan over time may help with overall adoption, so be open to the idea of ongoing engagement for long-term improvement. The governance and physician compensation committees, ideally staffed with both physicians and administrative stakeholders, are the best resources for plan development and adoption. They review the plan, identify outliers, and put into place policies and procedures to help support the values of the organization. There is a high-level of built-in trust with this model as those developing and implementing the plan understand the unique complexities associated with being a physician.

CD: Along those lines, communicate that this is not a “once and done” plan. Physicians will have a greater appreciation for the plan and process knowing that there will be an ongoing review process and a willingness to make changes as necessary. Let physicians know that you understand the bigger picture and that as health care evolves, the compensation program will need to flex over time to align with these changes.

Why and how can technology be used to support this effort?

CD: Change is often perceived as happening too fast. Having the use of technology to enable that change, especially when it comes to communicating and administering the plan, is key to its success. In this age of viral communications, things can spiral out of control quickly. We cannot rely on wRVUs to improve performance, nor can we rely on spreadsheets as a way to communicate and administer physician compensation. To engage physicians and gain trust when tying new non-productivity measures to compensation, organizations need to provide them with one place to access clear and concise performance data.

MR: Being able to show physicians all the components that impact their pay is key. You need to be clear about how the plan is structured, what components are being measured, the goals of the organization, what is expected from providers, the source of your reported data and the actual compensation calculations. Technology can provide a platform that is both accurate and transparent – allowing people to really see and understand how their compensation is tied to value. Many organizations are now accessing and assembling compensation data from multiple different systems, which is timeconsuming and can lead to human error. Data-driven technology transforms a lengthy and arduous process into one system that provides actionable insight and allows physicians and their managers to see as much or as little information as they want. This level of transparency creates an opportunity for course correction if needed.

CD: A strong technology platform can really act as the cornerstone for change. Just as EMRs have improved patient care, diagnostics, patient outcomes, and practice efficiencies, provider performance technologies can support organizations in the transition from volume to value by aligning pay with performance and serving the diverse needs of leadership, administrators and physicians.

SullivanCotter’s Provider Performance Management TechnologyTM

Provider Performance Management TechnologyTM (PPMTTM) is a market-leading, cloud-based solution that enables provider engagement through transparent performance-based compensation administration and analytical capabilities.

Utilizing best-in-class technology and decades of physician compensation and health care expertise, PPMTTM is designed to support organizations in the transition from volume to value. PPMTTM is offered as part of a comprehensive portfolio of advisory, information and technology services to address client needs.

John Putnam Joins SullivanCotter’s Executive Workforce Practice

SullivanCotter Welcomes New Principal, John Putnam

Jun. 19, 2018 – Minneapolis – SullivanCotter, the nation's leading independent consulting firm in the assessment and development of total rewards programs and workforce solutions for the health care industry and not-for-profit sector, welcomes new Principal, John Putnam, to the firm's Executive Workforce Practice.

Jun. 19, 2018 – Minneapolis – SullivanCotter, the nation's leading independent consulting firm in the assessment and development of total rewards programs and workforce solutions for the health care industry and not-for-profit sector, welcomes new Principal, John Putnam, to the firm's Executive Workforce Practice.

John is an emerging leader in the field with more than a decade of health care consulting experience, and serves as a trusted advisor to many of the nation's top hospitals and health systems. He works closely with not-for-profit health care organizations to align executive pay, performance and talent strategy with overall business goals – helping clients to remain competitive, agile and adaptable in an increasingly complex marketplace.

"In order to address the industry's new value-based performance goals and guidelines, executives are now tasked with measuring and assessing performance across the care continuum, developing targeted approaches to improve quality and patient outcomes, and working towards the advancement of overall organizational objectives. John has many years of experience in designing executive compensation strategies to support these goals, and will play a vital role in helping our clients to engage leadership in driving incremental change and helping to deliver long-term, sustainable results," said Ted Chien, President and CEO, SullivanCotter.

As the transition to value-based care intensifies, John specializes in the development of competitive executive total rewards programs, including both short and long-term incentives, tailored to the unique needs of each organization. He advises boards and compensation committees on best practices in governance to help ensure regulatory compliance, reasonableness and appropriate oversight of executive pay and benefits, and works closely with organizations to implement effective recruitment, retention and engagement practices.

Prior to joining SullivanCotter, John was a Senior Principal in Korn Ferry Hay Group's Executive Compensation Practice, where he worked primarily with health care board members and management on the design, administration and governance of executive pay programs.

About SullivanCotter

SullivanCotter is the leading independent consulting firm in the assessment and development of performance-based total rewards programs and workforce solutions for the health care industry and not-for-profit sector. For over 25 years, the firm has provided unbiased advice to executives and boards to help attract, retain and motivate executives, physicians, advanced practice providers and employees at all levels. Through the Center for Information, Analytics and Insights, SullivanCotter has developed the most widely recognized compensation surveys in the United States. Combining data-driven intelligence with national insights, we act with integrity to help organizations fulfill their missions, business objectives and regulatory requirements.

Contact: Becky Lorentz

SullivanCotter

beckylorentz@sullivancotter.com

314.414.3719

PODCAST | Governing Health - Director Compensation in Nonprofit Health Systems

Health care executive compensation trends

In an industry that continues to undergo unprecedented change, the role of the nonprofit health system director is now more important than ever. Engaging employees at this level is a major concern as their scope of responsibility grows more complex. In a seller's market for director services, devising competitive compensation packages is critical and can be used as a key talent development, recruitment and retention tool.

In the most recent edition of the Governing Health Podcast Series, Michael Peregrine, Partner, of law firm McDermott Will & Emery, welcomes two of the leading voices on executive compensation trends and practices in health care: Ralph DeJong, Partner, McDermott Will & Emery and Tim Cotter, Chairman and Managing Director, SullivanCotter.

LISTEN TO THE PODCAST

Modern Healthcare | Higher Stakes: Boards Play Pivotal Role in Hospital Direction

Evolution of the health care boardroom

As hospitals and health systems learn to navigate an increasingly consumer-driven marketplace for health care, the scope of the board's responsibility continues to expand in kind.

To help organizations align with the industry's new value-based performance goals and guidelines, trustees are now tasked with providing greater insight into emerging areas of focus such as consumer engagement, data analytics, information security and recruitment and retention.

Featured in the June 4th edition of Modern Healthcare, SullivanCotter discusses the evolution of boardroom activities from traditionally transactional into something much more complex.

In addition to overseeing executive compensation programs, boards are also taking the lead on other important issues such as cultural integration, leadership diversity, pay equity and more. Many are even diving deep into performance benchmarking and analyzing key quality metrics to help ensure alignment with and progress towards overall organizational goals.

REAL FULL ARTICLE

Fundraising Talent Strategy in 2018 and Beyond

Attract and retain high-performing fundraising professionals

As the saying goes, you need money to have a mission. Whether through in-kind donations or the receipt of funds from public or private sources, most not-for-profit organizations rely to some degree on philanthropy to obtain the funds needed to sustain their mission.

For some not-for-profits, the fundraising professionals vital to this process are considered the lifeblood of the organization, and the loss of key talent could mean a loss of momentum and/or continuity in donor relationships. In today’s environment, these organizations are also faced with the decline of both governmental and non-governmental funding sources and, in the wake of the Tax Cuts and Jobs Act (which doubled the standard deduction and will result in fewer itemized returns through which tax-deductible donations are claimed), a reduced incentive to donate. Attracting and retaining people with the critical skill set to perform fundraising successfully has become arduous as not-for-profit organizations face these realities, along with costs of replacing talent as high as 100% of salary in as often as every 18 months.

In developing a fundraising talent strategy for this year and beyond, consider proactive strategies to attract and retain high-performing and high-potential professionals, while also enhancing the capabilities of existing staff. Immediate efforts should focus on:

Auditing the skills and capabilities of the existing team

Complete a skills assessment to ensure the development office includes the types and number of staff necessary to achieve its goals. These types of assessments often reveal the need for:

- Different or additional leadership with the ability to cultivate meaningful relationships among donors and the leadership skills to grow and develop talent. Accomplished fundraising professionals will be drawn to and remain at an organization where leadership in this area is strongest.

- Innovative donor research capabilities and advanced donor analytics to ensure effective data mining. These skill sets can be developed in-house or outsourced.

- Advanced social media expertise. Branding and marketing in the era of social media presents increasingly sophisticated and unique ways to share the organization’s mission with potential donors. Ensure the right resources are in place to keep pace with the market.

Evaluating and expanding recruiting practices

Changes may not be needed for organizations that have identified proven strategies to attract top fundraising talent who stay for more than three years. However, it is worth considering that a tighter labor market for fundraising professionals may require a different approach to sourcing talent:

- For larger organizations, the market for top fundraising executives is primarily national in scope. Other fundraising positions are commonly recruited locally or regionally, though the market segments from which talent are drawn appears to be evolving.

- Universities that have historically looked only to higher education to draw talent are now recruiting fundraising staff from large health systems. Large health systems, in turn, are now including universities and other organizations—such as large charities—in the search for talent.

Evaluating the effectiveness of the compensation program

This is an important consideration, particularly in an environment where certain organizations have become increasingly aggressive in their efforts to recruit and retain high-caliber fundraising professionals.

An important first step in the evaluation of the program is to identify a compensation strategy that will support the organization’s current and anticipated recruitment, retention and performance objectives. Advanced compensation vehicles such as retention plans and/or deferred compensation arrangements may be needed to maintain a competitive edge in today’s market. Implementing such changes may represent a shift in culture and practice that will need additional socialization and buy-in from key stakeholders.

Providing performance-based pay in the form of incentives is legally permissible and more prevalent than ever. Organizations that offer incentives find that these programs can help to:

- Motivate people and teams to meet or exceed fundraising targets. This often requires a “both/and” approach of increasing revenue through effective fundraising strategies and operating more efficiently to reduce costs.

- Improve teamwork and collaboration. In some cases, the introduction of incentives brings a new discipline around fundraising that engages more staff in the development of strategies for securing new donors.

- Limit the amount of fixed costs. Since incentives are paid only when goals are met or exceeded, including incentives in the mix of pay provides a self-funding feature. From an optics perspective, the organization promotes a performance-based culture and demonstrates the sound management of fixed costs. Incentives are no longer considered lavish or unusual. Rather, they are a necessary component of a well-designed compensation strategy.

- Reinforce a culture of performance and accountability. The plan will be most effective when all team members are held to rigorous goals, develop strategies and operating plans by which to meet them, and work together to accomplish results.

- Address gaps in performance areas. After conducting a performance benchmarking study to identify gaps that may exist with respect to various fundraising targets (e.g., total funds raised, number of donors, transformational gifts received, cost per dollar raised), incentives can redirect efforts to fill those gaps.

Increase the focus on — and funding of — talent development strategies

Many organizations provide only basic opportunities for growth and limit talent development budgets in the spirit of cost-saving. By increasing the dollars allocated to skills building and the professional development of fundraising talent, the return on investment can be multifold and differentiate an organization in the minds of prospective and current development staff.

A thoughtful and disciplined approach to the activities outlined above can lead to dramatically improved attraction and retention in a highly-competitive market for fundraising talent. When deploying any new strategy, the key to a successful outcome lies in the design, implementation and communication efforts surrounding the strategy. In advance of proposing modifications to a current approach, traditional wisdom applies: include key stakeholders in the process, consider both current- and future-state needs as plans are developed, and assess the impact of any anticipated program changes. Ultimately, a program that successfully attracts and retains fundraising talent is one that is marketcompetitive, cost-effective, engaging and reinforced as a strategic differentiator for talent both inside and outside of the organization.

PODCAST | Governing Health - Executive Compensation Trends Update

With the new provisions set forth by the Tax Cuts and Jobs Act and recent trends associated with pay equity, the use of clawbacks and the expansion of incentive compensation goals and objectives, the governance of executive compensation remains a critical boardroom concern.

In the most recent edition of the Governing Health Podcast Series, Michael Peregrine, Partner, of law firm McDermott Will & Emery, welcomes two of the leading voices on executive compensation trends and practices in health care: Ralph DeJong, Partner, McDermott Will & Emery and Tim Cotter, Chairman and Managing Director, SullivanCotter.

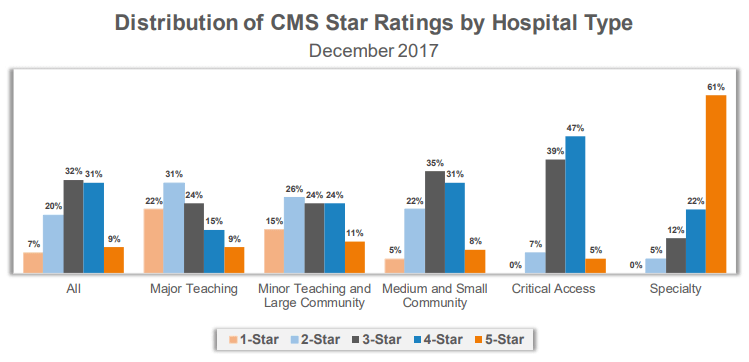

CMS Star Ratings Highlight Need to Compare Performance by Hospital Type

Understanding what drives performance

As the marketplace for health care grows increasingly complex, organizations must develop a greater understanding of what drives performance to remain competitive.

The Centers for Medicare and Medicaid Services (CMS) recently published its newest Star Ratings, designed to measure and report hospital quality. These ratings have provoked a number of questions and concerns as more than 3,600 hospitals - regardless of size, breadth of services, or geographic location - are benchmarked against a collective average.

SullivanCotter was recently featured in a Modern Healthcare article which addresses these differences. As organizations use these ratings to help drive improvement efforts, it is important to consider the following:

- Using national benchmarks like the CMS Star Ratings can be a great way for hospitals nationwide to help drive quality improvement, but only if they understand the nuances and complexities in the data and how to best analyze it.

- Not all hospitals are the same. To truly identify areas of meaningful improvement, hospitals must be compared to like hospitals.

- Organizations cannot improve what they cannot measure, and the new CMS Star Ratings continue to provide transparency in health care quality and performance as the industry shifts from volume to value.

- To drive improvement efforts and help organizations more effectively benchmark performance against their direct peers, the market requires a standard set of national quality metrics that is stratified by hospital type.

READ THE FULL ARTICLE

Using CMS Star Ratings to Drive Improvement at Specialty Hospitals

Using national benchmarks to drive quality performance

DOWNLOAD FULL ARTICLE

In order to remain competitive in an increasingly complex marketplace, health care organizations must develop a greater understanding of what drives performance and improves outcomes in the transition from volume to value. Although the overall aim to enhance patient satisfaction, improve quality and reduce the cost of care is the same, specialty hospitals, academic medical centers, community hospitals, and major and minor teaching hospitals each operate under very distinct circumstances.

The conditions they treat are as different as the populations they serve and it cannot be assumed that patient experience at one type of hospital will be commensurate with the other. The Centers for Medicare and Medicaid Services (CMS) published its most recent Star Ratings in December 2017. While designed to measure and report hospital quality, these ratings have provoked a number of questions and concerns as more than 3,600 hospitals - regardless of size, breadth of services, or geographic location - are benchmarked against a collective average. The complexities and nuances of the new ratings can make it difficult for hospitals to truly understand how they compare to their peers and where there are still opportunities for improvement.

CMS defines specialty hospitals as those that are primarily or exclusively engaged in the care and treatment of patients with a cardiac condition; patients with an orthopedic condition; or patients receiving a surgical procedure. While CMS bases these ratings on 57 different quality measures across seven areas of performance, specialty hospitals only reported an average of 27.2 of the 57 measures. For example, 97% of specialty hospitals reported patient experience metrics. On the other hand, only 5% of specialty hospitals reported data on acute ischemic stroke 30-day mortality and 30-day readmissions because they do not typically treat this condition.

The same is true for patients with complex medical conditions such as pneumonia, coronary artery bypass graft, chronic obstructive pulmonary disease and acute myocardial infarction. Only 20-25% of specialty hospitals that were rated included measures for mortality and/or readmissions for this patient population. Additionally, less than 25% of specialty hospitals reported data for the majority of the NHSN infection rates in the Safety of Care measure group, excluding C. Difficile. The CMS ratings require additional stratification by hospital type in order to paint a more accurate picture regarding how organizations are performing in relation to their direct peers.

However, the impact of further stratification could be significant for specialty hospitals as 83% of the 74 specialty hospitals included received a four- or five-star rating. With a small number of metrics to report, specialty hospitals have fewer variables to address to help improve their scores within this ranking system and, more importantly, the care delivered to patients that can be benchmarked with publicly-reported data. All hospitals, including specialty hospitals, need to understand their variation to national benchmarks as well as the variation to their peers.

Specialty hospitals using CMS Star Ratings to drive improvement efforts should focus on the following steps:

DEFINE YOUR PEER GROUP

In addition to reviewing benchmarks for like hospitals, specialty hospitals must also consider how their ratings compare to other relevant local and regional competitors. Patient experience scores, for example, can vary widely by region. As the highest weighted measure in the CMS Patient Experience group, “Overall Rating of Hospital” had a national average of 89.01 in the December 2017 Star Ratings. On average, Nevada hospitals show a linear score of 86.90 while Wisconsin hospitals show a linear score of 90.78 - a 4.5% difference between the two states. Regional differences are important to consider when evaluating performance compared to a set of benchmarks.

BENCHMARK YOUR PERFORMANCE AGAINST PEERS

Do not underestimate the importance of peer group selection. Not all hospitals are the same – and to truly identify areas of meaningful improvement, hospitals must be compared to like hospitals. Hospitals will often have more than one peer group. For example, a specialty orthopedic hospital will want to benchmark itself against other orthopedic hospitals. However, it might also want to benchmark specific metrics like patient experience against other local hospitals that offer orthopedic services.

IDENTIFY AREAS FOR IMPROVEMENT

It is critical that organizations develop a better understanding of their variation to the CMS benchmarks. If a specialty hospital is performing above or below average, the key is to identify ‘how’ and ‘why’. Individual metrics that have a negative variance to peer group benchmarks highlight potential opportunities for improvement. Additionally, identifying areas that are important to patient outcomes and the mission of your organization will resonate most with staff and have a higher likelihood for improvement.

ALIGN REWARDS WITH TARGETED IMPROVEMENTS

Once an organization selects a specific area to target in improvement efforts, it is important to determine how employees can be motivated or incentivized to engage in these activities. As organizations shift from volume to value, quality metrics are becoming more prevalent in provider compensation plans. For example, according to SullivanCotter’s Physician Compensation and Productivity Survey, quality incentive compensation for physicians increased in 2017 from an average of 5.9% to 7.4% of total cash compensation. Aligning quality improvement efforts with compensation is an effective approach to driving change and helping to reach overall organizational goals.

REEVALUATE REGULARLY

While it is difficult to generate significant progress on one metric in a single year, organizations should not overlook the need to review these benchmarks in aggregate on a periodic basis. If there is a noticeable shift in the data, changing direction and adjusting improvement efforts accordingly is important.

CMS Star Ratings continue to provide transparency in health care quality and performance as the industry maintains its focus on value-based care. Perhaps the adage that best applies is “you can’t improve what you can’t measure” - and these ratings are certainly a step in the right direction. Despite the myriad of differences in the 3,600+ hospitals included in the CMS ratings, all share a common goal of advancing the overall quality of health care. However, to truly drive improvement and help organizations more effectively benchmark performance, the market requires a standard set of national quality metrics that is stratified by hospital type.

Organizations like the National Quality Forum and others are helping to establish these national benchmarks. Standardizing the process would help to facilitate more meaningful comparisons, allowing specialty hospitals to focus more on individual opportunities for improvement and less on their variance from the collective national average.